Key Takeaways

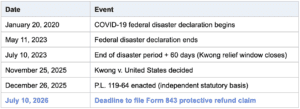

- A November 2025 federal court ruling held that COVID-19’s federal disaster declaration automatically suspended IRS filing and payment deadlines from January 20, 2020 through July 10, 2023 — a 3.5-year window, far longer than the IRS’s administrative relief.

- Refund eligibility is broad: Individuals, businesses, trusts, estates, and nonprofits who paid federal failure-to-file penalties, failure-to-pay penalties, underpayment interest, or estimated tax penalties tied to deadlines in that window may be entitled to relief.

- The deadline to file Form 843 is July 10, 2026. Kwong tolls the normal IRC § 6511 statute of limitations, but only until that date.

- A protective claim preserves your rights while the DOJ’s expected appeal plays out. Not filing forecloses any refund; filing costs little.

Bottom Line: Any taxpayer who paid federal penalties or interest on a return or payment due between January 20, 2020 and July 10, 2023 should evaluate a protective Form 843 claim before July 10, 2026.

The Kwong Decision and IRC § 7508A(d)

In Kwong v. United States, 179 Fed. Cl. 382 (Nov. 25, 2025), the U.S. Court of Federal Claims interpreted the pre-2025 version of IRC § 7508A(d) — the provision that postpones federal tax deadlines during a federally declared disaster. The court held that the COVID-19 disaster declaration triggered an automatic suspension of filing and payment deadlines that ran the full length of the declared disaster period, which ran from January 20, 2020 through July 10, 2023 (May 11, 2023 plus 60 days). The IRS’s administrative COVID relief covered only narrow slices of that time. Kwong says the statute covered all of it.

In the court’s own words: “The plain meaning of that statute is that the automatic extension runs from the beginning of the disaster declaration, through the end of the declared disaster period, and until 60 days after the end of the declared disaster period.”

Who Is Eligible for a Refund?

Eligibility is unusually wide. Because COVID-19 was a nationwide disaster declaration — not a county- or state-specific FEMA event — the geographic qualification is met for virtually every U.S. taxpayer.

That includes:

If you paid any of the following between January 20, 2020 and July 10, 2023, you should evaluate a claim:

- Failure-to-file (FTF) penalties on returns due between January 20, 2020 and July 10, 2023

- Failure-to-pay (FTP) penalties assessed during the same window

- Underpayment interest that accrued during the disaster period

- Estimated tax penalties (IRC § 6654) where the due date fell within the window

- Interest and penalties accrued during the period even where the underlying liability pre-dated January 20, 2020 (partial relief may apply)

Why the Filing Deadline Has Not Yet Passed

Under normal rules, IRC § 6511 requires refund claims to be filed within the later of three years from the date the return was filed or two years from the date the tax was paid. For most pandemic-era tax years, that window has already closed.

Kwong changes the math. The decision requires the entire COVID disaster period (Jan. 20, 2020 – Jul. 10, 2023) to be disregarded when computing the limitations period. In practice, this tolls the statute of limitations by the length of the disaster window — pushing the effective deadline out to July 10, 2026 for most affected taxpayers.

Miss that date, and the door closes.

How to File a Protective Refund Claim Under Kwong

The vehicle is Form 843, Claim for Refund and Request for Abatement.

A protective claim should include:

- A written legal statement identifying Kwong v. United States as the basis for the claim, plus the alternative statutory basis in P.L. 119-64 (enacted December 26, 2025), which independently requires the IRS to treat disaster-period postponements as extensions of return deadlines for refund lookback purposes. Citing both gives the IRS two independent grounds to grant relief.

- Identification of the specific tax year, penalty type, and amount paid.

- Supporting documentation — IRS notices, account transcripts, or canceled checks evidencing the payment.

- Certified mail submission before July 10, 2026, to establish a record of timely filing.

A properly filed Form 843 preserves the taxpayer’s right to a refund even if the legal landscape shifts during appeal.

Important Caveats Before You File

Appeal risk. The Department of Justice is widely expected to appeal Kwong to the Federal Circuit. The decision is not yet final. A protective claim preserves your position while the law settles.

Federal only. Kwong interprets the Internal Revenue Code. It does not automatically extend to state-level penalty or interest assessments — New Jersey, New York, and other state tax authorities operate under separate statutes and may not honor the federal disaster tolling.

No guaranteed refund. Filing Form 843 does not guarantee the IRS will pay. The IRS may hold protective claims in suspense pending final legal resolution. But not filing guarantees no refund.

Documentation matters. The strength of a Kwong claim turns on the paper trail — what was paid, when, and against which assessment. Cleaner records mean cleaner claims.

Frequently Asked Questions

Does Kwong apply to my state tax penalties?

No. Kwong interprets federal disaster postponement law under IRC § 7508A. State tax agencies set their own deadlines and disaster relief rules.

I already paid IRS penalties for a 2020 or 2021 return. Is it too late?

Likely not. The Kwong tolling pushes the refund claim deadline to July 10, 2026 for most taxpayers with deadlines that fell inside the disaster window.

What if my underlying tax liability pre-dated COVID?

You may still recover interest and penalties that accrued during the disaster period, even if the original liability arose before January 20, 2020.

Will the IRS just deny my claim because of the appeal?

The IRS may hold protective claims in suspense. That is a feature, not a problem — it keeps your position alive until the law is final.

Do I need a tax professional to file Form 843?

You can file on your own. But a properly drafted legal statement citing both Kwong and P.L. 119-64, plus a documented audit trail, materially improves the odds of a successful refund.

Key Dates at a Glance

Next Step: Don’t Let July 10, 2026 Pass Without a Decision

If you or your business paid federal penalties or interest tied to a deadline between January 20, 2020 and July 10, 2023, the window to act is closing. A protective Form 843 claim is a low-cost way to preserve potentially significant refunds while the appellate process runs its course.

Wiss’s tax advisory team is reviewing client accounts for Kwong-eligible refunds and preparing protective claims on a case-by-case basis. If you’d like us to evaluate whether you have a claim worth filing, contact a Wiss tax advisor before the July 10, 2026 deadline.